How Construction Bond Rates Are Determined

Understanding how construction bond rates are determined is crucial for any contractor looking to bid on public or large private projects. It’s not a simple, one-size-fits-all calculation. Instead, surety companies engage in a rigorous underwriting process, essentially a detailed risk assessment of the contractor’s business. They carefully evaluate a contractor’s financial health, operational experience, and overall reliability to determine the likelihood of a claim being made against the bond. This process is foundational to the surety-contractor relationship and directly impacts the bonding cost.

Surety underwriters often refer to the “Three C’s of Credit” when assessing a contractor. This framework allows them to build a holistic picture of the contractor’s ability to complete a project and meet all financial obligations successfully.

- Capital refers to your financial strength and is arguably the most scrutinized aspect. Underwriters look at key figures like working capital (current assets minus current liabilities), net worth, and overall cash flow. Substantial working capital demonstrates your ability to manage day-to-day operational costs, such as payroll and materials, without strain. A healthy net worth provides a cushion to absorb potential losses or unexpected project costs. Underwriters also analyze your company’s debt-to-equity ratio and retained earnings, which show a history of profitability and sound financial management. In many cases, especially for closely-held companies, the personal financial strength of the owners is also considered, as they will be required to indemnify the surety company personally.

- Capacity: This is your operational ability to perform the work specified in the contract. Underwriters assess this by reviewing your company’s history, including the size, scope, and complexity of previously completed projects. They want to see a track record of success on jobs similar to the one being bonded. They also evaluate your resources, including the experience of your key personnel (project managers, superintendents), the availability of necessary equipment (both owned and rented), and your established relationships with reliable subcontractors. Your current backlog of work (work-in-progress) is also analyzed to ensure you are not overextended and have the capacity to take on a new project without compromising existing ones.

- Character: This encompasses your company’s reputation, integrity, and history of meeting obligations. It’s about demonstrating that you are a trustworthy business partner. Underwriters will check references from past project owners, architects, and engineers. They will also look at your payment history with suppliers and subcontractors, often by reviewing credit reports and trade references. A long history of completing projects on time, within budget, and paying all bills promptly speaks volumes. Conversely, a history of litigation, liens, or previous bond claims can be a significant red flag and may lead to higher rates or even a denial of bonding.

Surety companies, acting as specialized insurance providers, thoroughly evaluate these factors before issuing bonds. When your profile reflects strength and reliability in these areas, the perceived risk decreases, leading to more favorable and competitive rates. Maintaining a solid financial and professional standing can make a significant difference in securing the best possible terms for businesses or individuals seeking affordable surety bonds Texas.

To facilitate this assessment, underwriters typically require a comprehensive package of documents. These might include:

- Financial statements (balance sheets, income statements, statement of cash flows) for the past three years

- Work-in-progress schedules

- Completed contract schedules

- Bank references and letters of credit

- Resumes of key personnel

- Project references

- Organizational charts

What is a Construction Bond Rate?

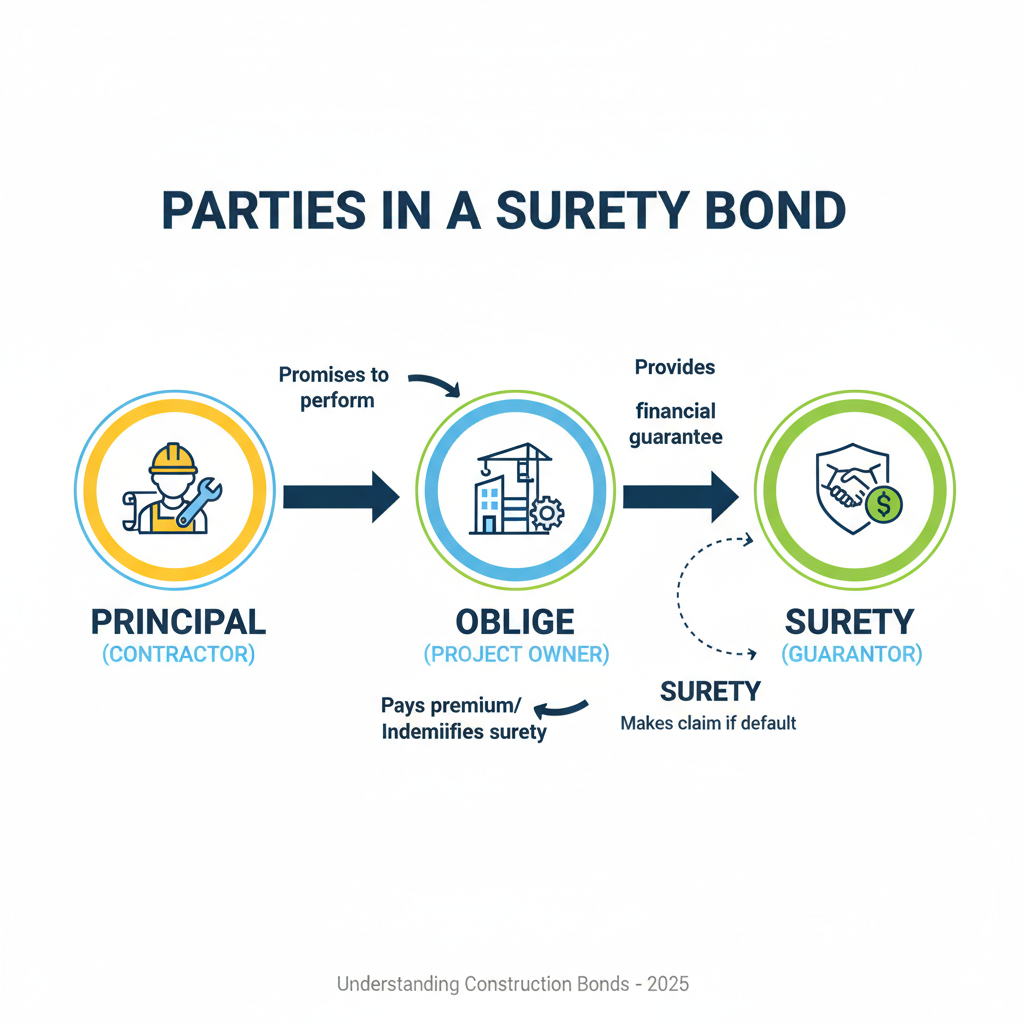

At its core, a construction bond rate is the percentage a surety company charges for providing a bond. This percentage is applied to the total bond amount (often the full contract value) to calculate the premium you will pay as the contractor. It’s essentially the cost of the guarantee the surety provides to the project owner (the obligee), ensuring that the project will be completed and all laborers and suppliers will be paid according to the contract terms.

This rate is not arbitrary; it culminates the surety’s detailed underwriting and risk evaluation. Factors such as the contractor’s financial stability, past performance, the specific type of bond required (e.g., performance, payment, bid), and the project’s characteristics all feed into this calculation. A lower rate indicates a lower perceived risk, reflecting the surety’s confidence in your ability to fulfill your contractual obligations without issue.

The Difference Between a Bond Rate and a Bond Premium

While often used interchangeably in casual conversation, there’s a clear and vital distinction between a bond rate and a bond premium.

The bond rate is the percentage used to calculate the bond cost. It’s the multiplier determined by the surety’s underwriting process. For instance, a surety might quote a well-qualified contractor a rate of 1% for a standard performance bond.

The bond premium is the actual dollar amount you pay for the bond. It results from applying the bond rate to the required bond amount. This premium is the fee for the surety’s service and guarantee for the project’s term.

Let’s illustrate with an example: If you need a $100,000 performance bond for a project, and the surety company quotes you a bond rate of 1%, your bond premium would be $1,000 ($100,000 x 0.01). This $1,000 is the total cost to secure that bond for the specified term. This premium is typically paid upfront and is considered fully earned by the surety, meaning it is generally non-refundable even if the project is completed early or canceled.

Key Factors That Influence Your Bond Rate

Many elements come into play when a surety company determines your construction bond rate. These underwriting factors can be broadly categorized into your qualifications as a contractor and the specific details of the project you’re undertaking. A thorough understanding of these factors can empower you to take steps to secure the most favorable rates possible.

The Role of Credit Scores and Financial Health

Your personal and business financial health is arguably the most significant factor influencing your construction bond rate. Surety companies view bonds as a form of credit; if a claim is paid out, you are ultimately responsible for reimbursing the surety. Therefore, your financial reliability and stability are paramount.

- Personal Credit Score: Your credit score is a primary indicator of your financial responsibility for many bonds, especially for smaller contractors or new businesses. A strong score (typically above 700) signals that you manage your finances well and are less likely to default on obligations.

- Business Credit: Beyond personal credit, the financial standing of your business is scrutinized. This includes your company’s net worth, working capital (current assets minus current liabilities), and consistent positive cash flow. These metrics demonstrate your business’s ability to operate profitably, manage its short-term obligations, and withstand financial pressures like a delayed payment from a client.

- Financial Statements: The quality and transparency of your financial statements are critical. Underwriters consider a hierarchy of assurance. Internally compiled statements offer the least assurance. CPA-prepared financials are strongly preferred, with reviewed statements offering limited assurance and audited statements providing the highest level. Audited financials, prepared by a construction-focused CPA, give the surety the utmost confidence in the accuracy of your financial position. These documents provide a comprehensive snapshot of your company’s financial stability. Understanding how your financial standing impacts your ability to secure various forms of credit is essential for effectively managing your business’s borrowing capacity and bond rates.

For contractors with excellent credit and strong, audited financials, rates can be as low as 0.5% to 1.5% of the contract value. Conversely, a weaker financial profile, poor credit, or internally prepared financials will typically lead to higher rates, often in the 2.5% to 5% range, or could even result in being declined for bonding.

Project Size, Complexity, and Type

The characteristics of the project itself also heavily influence bond rates. Surety companies assess the inherent risks associated with the scope of work, duration, and contractual obligations.

- Project Value: Larger contracts often benefit from tiered rates or a sliding scale, where the percentage rate decreases as the contract value increases. For example, a surety might charge 2.5% on the first $100,000 of a contract, 1.5% on the next $400,000, and 1% on the next $2,000,000. This structure reflects that while the total risk is higher on a larger project, the administrative costs of underwriting do not scale linearly.

- Project Duration: Longer projects inherently carry more risk due to potential economic shifts, material price fluctuations, labor market changes, and other unforeseen challenges that can arise over time. Projects exceeding a standard duration (e.g., 12-24 months) might incur a “time completion surcharge,” an additional premium to cover this extended risk period.

- Project Complexity: Highly specialized or complex projects, such as hospital renovations, data centers, or unique design-build contracts, may carry higher rates due to increased risk. For instance, design-build projects often incur a 20% to 50% surcharge on performance and payment bond premiums because the contractor assumes both the design liability and the construction risk.

- Type of Work: The nature of the construction work (e.g., heavy civil, commercial vertical, residential, environmental remediation) also plays a role. Each type has its own risk profile. For example, underground utility work can have more unforeseen risks than standard above-ground commercial construction, which underwriters factor into their rate filings.

Furthermore, a project’s geographic location can introduce unique risks, from local labor market conditions to specific state regulations. The surety market can vary by state; for example, contractors looking for Affordable surety bonds in Texas will find that local underwriters are attuned to the region’s specific economic climate and construction landscape, influencing rate availability.

Here’s a general comparison of typical costs for different bond types, though specific rates will vary based on the factors discussed:

Bond Type Typical Cost Range (as % of Bond/Contract Value) Notes Bid Bond Often a flat fee ($100 – $500) or free with a qualified surety relationship. Guarantees that the winning bidder will enter into the contract and provide the required performance and payment bonds. Performance Bond 0.5% – 2.5% for preferred rates; 2.5% – 5% for challenging accounts. Guarantees the contractor will perform the work according to the contract’s terms and conditions. The rate is applied to the full contract value. Payment Bond is often included with the performance bond premium at no extra cost. Guarantees that the contractor will pay all subcontractors, laborers, and material suppliers associated with the project. Supply Bond 0.75% – 3% of the supply contract value. Guarantees that a supplier will deliver materials or equipment as specified in their contract.